AI to Shape Indonesia’s Digital Economy as It Moves Toward USD 180 Billion 2030

27 Nov 2025

Indonesia’s digital economy is entering a critical transition period, with multiple reports indicating that the country will remain the largest and most dynamic digital market in Southeast Asia through the rest of the decade.

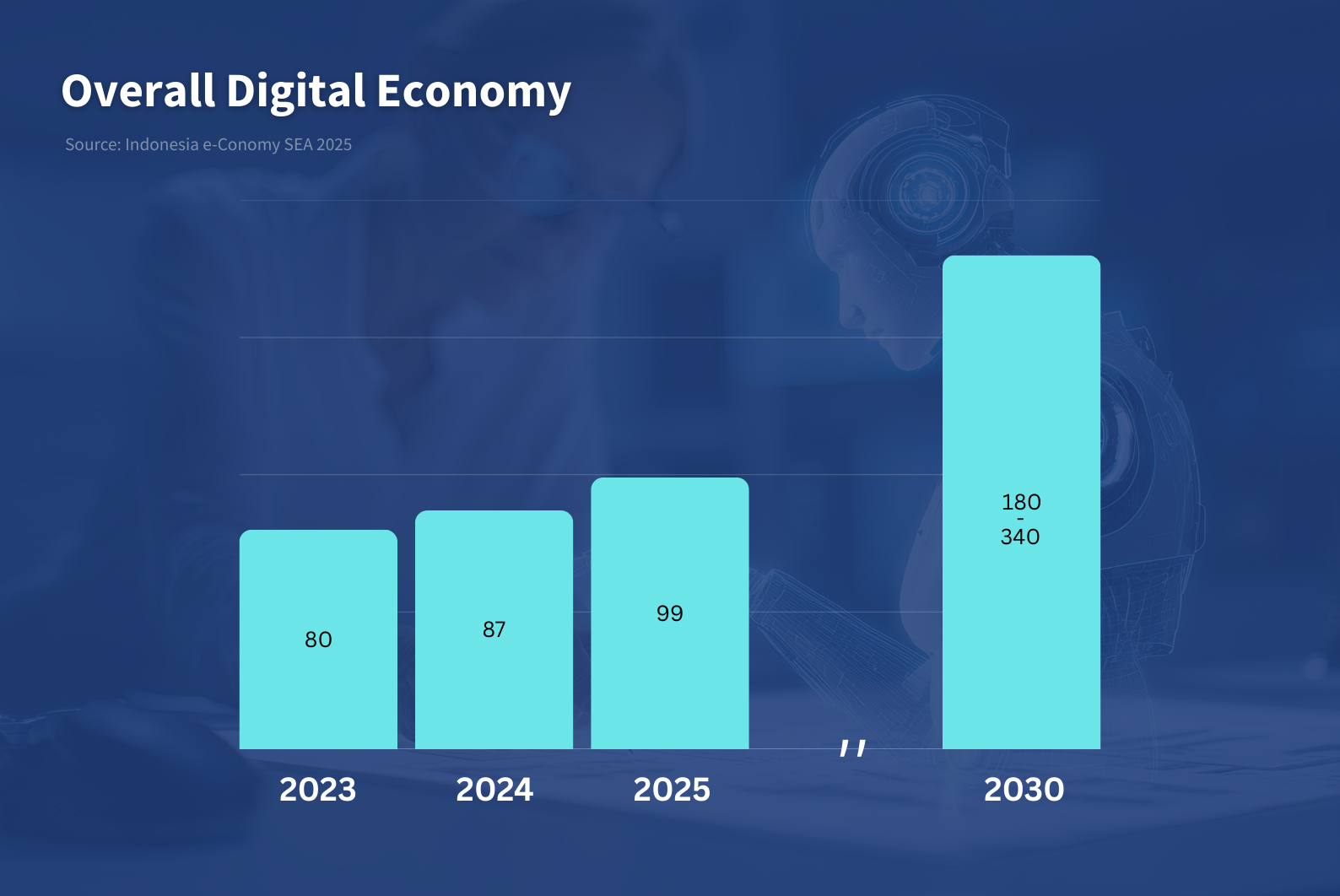

According to the e-Conomy SEA 2025 report by Google, Temasek and Bain & Company, Indonesia’s digital economy is approaching nearly USD 100 billion in gross merchandise value (GMV) by 2025, supported by resilient activity across e-commerce, digital financial services, video commerce and the accelerating integration of artificial intelligence (AI). While macroeconomic pressures have led Bank Indonesia to cut interest rates six times since September 2024 and the government to issue a USD 1.5 billion stimulus package, online sector expansion remains steady as consumer adoption deepens.

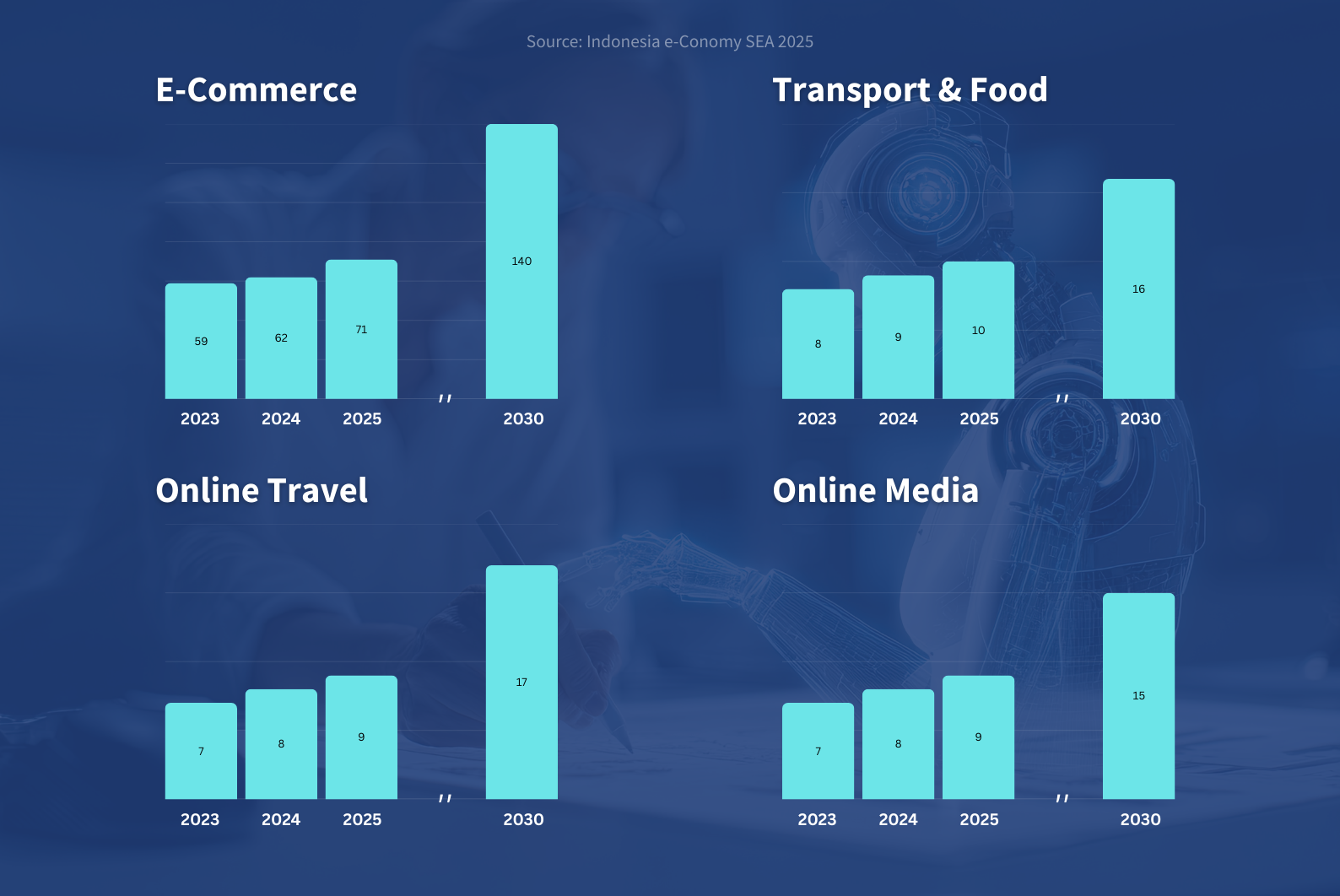

That adoption is most visible in e-commerce, which continues to dominate Indonesia’s digital landscape. GMV is projected to reach USD 71 billion in 2025, rising from USD 59 billion in 2023. A significant shift within this sector is the rapid rise of video commerce. The Indonesia country report shows that the number of sellers using video increased 75% year-on-year to 800,000, driving a 90% increase in transaction volume to 2.6 billion. Indonesia now leads Southeast Asia in both video commerce transactions and growth, particularly in fashion, beauty and personal care.

Source: Indonesia e-Conomy SEA 2025

Broader data from We Are Social’s Indonesia Digital Retail Outlook 2025 report reinforces this momentum: more than 220 million Indonesians — around 80% of the population — are online, and 95% use smartphones as their primary device. The report estimates that Indonesia’s e-commerce GMV surpassed USD 75 billion in 2024 and could move past USD 100 billion by 2026, supported by sustained demand in electronics, fashion, groceries, health and beauty, and home living.

This expanding consumer base is also shaping the country’s digital financial services (DFS), which are experiencing sustained double-digit growth. Digital payment GTV is projected to increase from USD 340 billion in 2023 to USD 538 billion in 2025, according to the Indonesia e-Conomy report, while digital lending could nearly double from USD 7 billion to USD 13 billion over the same period. Digital wealth and insurance continue to grow alongside the national QRIS payment system, which is promoting unified digital transactions nationwide. This financial activity aligns with We Are Social’s findings that more than 80% of urban consumers now rely on e-wallets for daily payment needs.

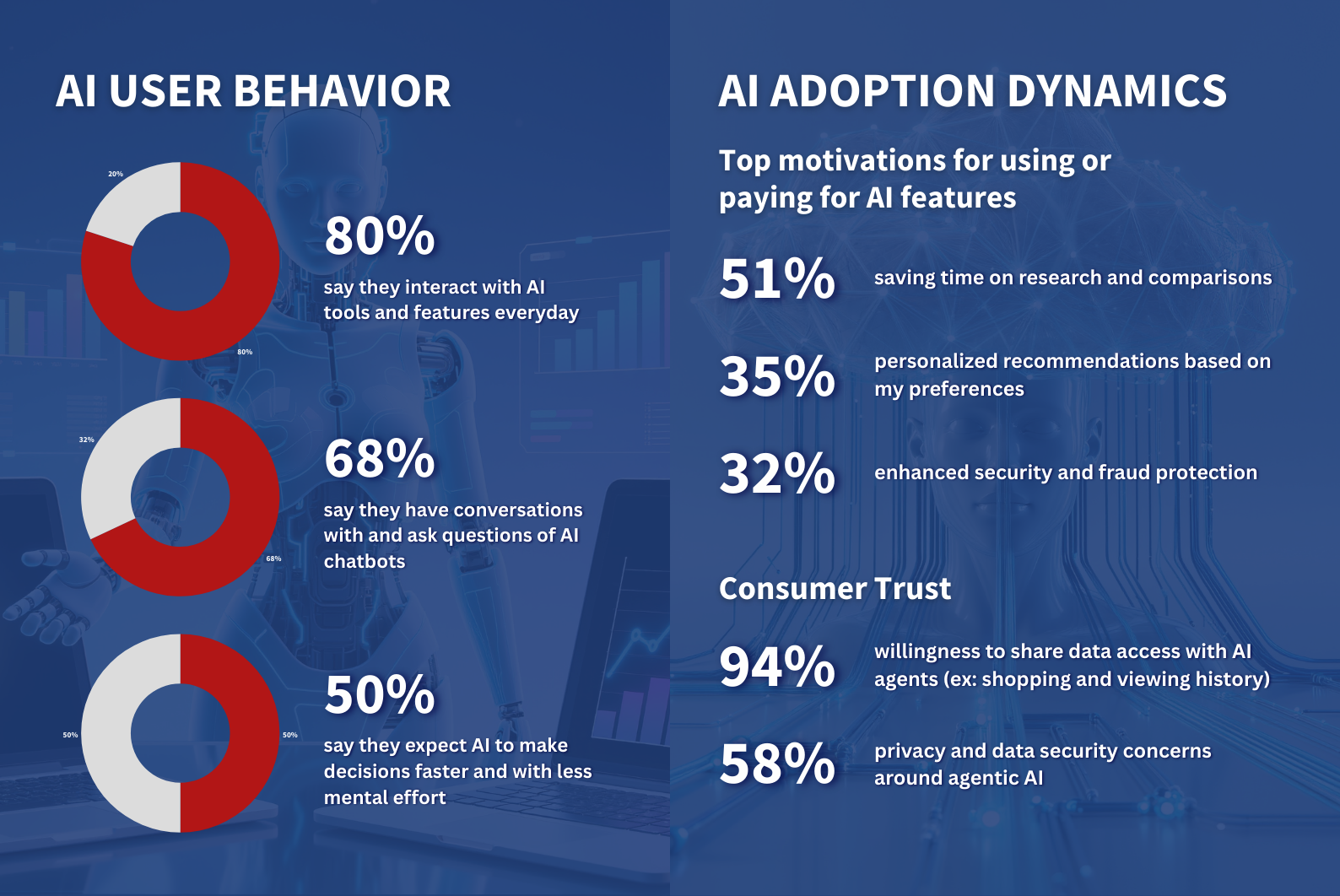

The increasing role of AI is beginning to influence the direction of these services. Indonesia recorded the strongest commercial momentum for AI applications in Southeast Asia, with revenue from AI-enabled apps growing 127% year-on-year — higher than any other market in the region. The e-Conomy SEA 2025 report notes that 79% of Indonesian users have learned to use AI tools, and daily engagement is becoming routine.

Source: Indonesia e-Conomy SEA 2025

These national trends reflect broader regional investment patterns highlighted by Google’s release accompanying the report, which states that Southeast Asia attracted more than USD 2.3 billion in AI-related funding over the past year, representing over 30% of private investment in early 2025. Indonesia captured 4% of ASEAN’s AI investments during this period, while more than 4,600 MW of new data-center capacity across the region is planned to support future AI demand.

That demand continues to grow despite a muted funding environment. Reuters’ summary of the e-Conomy report shows that Southeast Asia attracted USD 7.7 billion in private funding in the 12 months to June 2025 — up 15% year-on-year but still about 70% below the 2021 peak. Capital is increasingly directed toward late-stage deals, while early-stage rounds declined to about 20% of total deal flow. Digital financial services remain the largest recipient of private capital, and AI startups continue to attract consistent interest. Indonesia’s domestic funding climate, however, remains uneven, with the country-specific report indicating subdued investment in e-commerce, transport, online media and emerging sectors such as sustainability technology and Web3.

Uneven conditions are also reflected in local assessments of Indonesia’s digital outlook. CELIOS’s Indonesia Digital Economy Outlook 2025 projects modest 0.5% growth in e-commerce in 2025 due to weaker purchasing power and potential VAT adjustments. Digital payments and online lending, however, are expected to expand significantly, reaching IDR 2,908.59 trillion and IDR 365.70 trillion respectively. CELIOS analysts highlight persistent challenges, including regional disparities in digital infrastructure, a “tech winter” in funding, and rising cybersecurity exposure. Indonesia currently ranks 48th in the National Cyber Security Index, underscoring the need for more robust safeguards.

These considerations are becoming central as Indonesia implements major policy initiatives aimed at shaping the digital sector’s long-term trajectory. The U.S. Commercial Service notes that the 2022 Personal Data Protection Law, evolving AI guidelines, and data-localization regulations will continue to define operating conditions for both foreign and domestic firms. At the same time, government programs such as the National Strategy for Digital Economy Development (2023–2030), the National AI Strategy (2020–2045) and the “100 Smart Cities” initiative signal ongoing efforts to strengthen digital infrastructure, regulatory frameworks and public service digitization.

Taken together, these developments point toward a digital economy that could reach around USD 180 billion in GMV by 2030, according to the mid-range projections presented in the e-Conomy SEA 2025 report. While the upper-bound scenario extends to USD 340 billion, current conditions suggest that the more moderate path is likely to guide Indonesia’s progress. As AI adoption accelerates and platform innovation continues, Indonesia is positioned to remain a central driver of Southeast Asia’s digital landscape as the region transitions from a decade of digital expansion toward what the report identifies as an emerging “AI reality”.

RELATED ARTICLES

COMPANIES IN THIS SECTOR